For the best reading experience, read this newsletter online by clicking here!

If you’re reading this and not already a subscriber, then click on the button below and look forward to receiving these newsletters into your inbox every Monday.

Afternoon All,

Rishi announced this year’s budget this week. Whilst it was one of the more interesting budget reviews of recent years, it doesn’t warrant a full section in this newsletter, so have a read of this deep-dive to get a decent understanding of what happened.

The readers have also said that we need more photos in this newsletter, so I’ll see what I can do.

Onto the news.

Jack

We’ll get onto Greensill in a bit, but first let’s look at Jack Dorsey, the co-founder and CEO of both Twitter and Square.

Everyone will know what Twitter is by now, but for those that don’t know what Square is, it’s a mobile payments firm currently “blurring the lines between B2C and B2B, and giving small businesses a growing suite of e-commerce and financial tools”1. It’s a company that’s actually helping the backbone of this nation’s economy, so we’ve got to give them credit for that2.

Jack’s name has been a talking point recently as a result of Square’s questionable acquisition of a majority share of Tidal, the premium music streaming service part-owned by Jay-Z and a roster of other artists.

The deal has left more than a few people scratching their heads, as Square is neither in the music streaming business nor has it ever mentioned previously that it may try and diversify into the streaming business. At least from where I’m sitting, it really begs the question of ‘what possible rationale was behind this deal? What will Tidal bring to Square? Why now? Just why?’

It seems that Square shareholders were similarly confused by the announcement, as Square shares dipped 7% in the early moments of Thursday trading after the deal was shared with the wider world.

Jack, (as he is very used to doing3,) had to try and convey the vision that ultimately led to this deal happening on Twitter:

Once he lays it out like this you can kind of see where he’s coming from.

You could also look at it another way though.

As it’s no secret that Jack and Sean Carter are friends4, one could argue that this is just an example of one friend helping another out. If the idea of a revolutionary new artist platform works, then great, but if it ends up crashing and burning, then no one will be particularly annoyed either, as Square will continue being Square, and Sean will have run all the way to the bank with the cash and stock that was used to buy Tidal.

It’s chummy deals like these that shareholders really aren’t huge fans of, as it is irresponsible management plain and simple, and demonstrates a general disregard for other stakeholders. You can see why SilverLake and Elliott Management have been so obsessed with trying to remove Jack from his position at Twitter.

Hertz

You may remember that around the beginning of the first lockdown, Hertz (who was already in a very shaky financial position) declared bankruptcy.

I wrote about it back in June:

The car-hire group Hertz filed Chapter 11 bankruptcy proceedings on March 26th. This would traditionally push the market value of the company's equity downwards, as it becomes more likely that equity holders won't be entitled to as big a chunk of 'the pie' as they previously were (here's an explanation of Chapter 11). Retail investors in Hertz, however, saw a completely different picture. The share price of the bankrupt company rallied 887% in the 13-day period post-announcement, as investors banked on Hertz making it out of proceedings without reorganising its capital structure (which is kind of the whole point of Chapter 11).

Whilst all true, I think past me gave too much credit to the aforementioned ‘retail investors’, as with hindsight, it’s now quite easy to see that the movements in Hertz stock were a result of people just having some fun. There was no logic behind it. They weren’t making a nuanced distressed equity play. A lot of them just pressed ‘buy’ and the stock rocketed. Sound familiar?

So, what’s happened since then? Well, it was announced this week that Hertz’s equity holders are now going to be completely wiped out by the planned restructuring. This was a scenario that pretty much everyone saw coming back in April, and yet the retail crowd chose to ignore it5, and now here we are.

{kind=link}

Looking back though, what made this Chapter 11 particularly interesting was that Hertz tried to raise fresh equity back in June by means of an at-the-money (ATM) equity offering6, whilst in the midst of the bankruptcy. It was one of the first instances of ‘the establishment’ taking advantage of the irrational behaviour of the ‘stonks market’ that we currently find ourselves in. In this scenario, the offering was shut down by the SEC7 on the grounds that Hertz was effectively selling shares that they knew were worthless, simply because they knew that there was going to a retail trader on the other side of the trade willing to buy the shares. Hertz saw a way of raising up to $1bn in cash, that they knew would help pay those with more senior claims on the company, i.e. Hertz’s senior creditors.

If this kind of activity is ringing any bells for anyone, we’ve seen this kind of tactic again with AMC during the GameStonks saga. AMC sold 50m new shares in an at-the-money offering when the shares were ~$5, essentially helping the cinema operator avoid a messy bankruptcy by shoring up its cash reserves. Tesla also did an ATM offering in the weeks running up to it being added to the S&P 500. You can read more about this issuance here, as it’s pretty sneaky, even by Zach Kirkhorn standards.

And now for the section (I think), you’ve all been waiting for.

Greensill

Watching Greensill implode over the past week has been a surprise to be sure, but a welcome one8.

Greensill, the Softbank-backed supply chain financing firm announced its plans to go into insolvency today, after a week where pretty much everything that could have gone wrong, did go wrong.

Before we begin, it’s important to know a couple of things.

The first is that Greensill is headed up by Lex Greensill, an Australian farmer, turned law clerk, turned investment banker, and has spent the last decade at the helm of one of the most exciting and controversial businesses around. The second thing you (sort of) need to know is what supply chain finance is, as this may be the first time you’ve come across it.

Initially, understand that ‘factoring’ is the act of selling your receivables for a discount9 (I’ve gone into way more detail and explained the whole process in that footnote).

Reverse factoring, which is another name for supply chain finance, is, well, the reverse of it. The editorial board of the FT manages to explain it far better than I ever could:

“A buyer — often a large business — agrees with its suppliers that they will be paid by an intermediary [in this case Greensill], so they receive payments more quickly but at a small discount. The business later pays the full sum to the finance provider”

A lot of supply chain financing businesses stop at this point, but not Lex’s shop. Lex decided to be particularly commercial and went one step further, by choosing to securitise these cash flows by selling them to a special purpose vehicle (arranged by Credit Suisse), which then in part gets sliced up and sold onto investors (with the help of Credit Suisse Asset Management). You may have been able to deduce that Credit Suisse plays a large part in this whole arrangement, as well as the fact that this kind of thing is ever so slightly sketchy (find out why here).

This is really complicated stuff, so if you’re not on board then don’t worry.

This brings us to last Monday when we got word that Credit Suisse pulled the plug on Greensill and froze investor accounts after a ‘partial pullback by Greensill’s insurers10’. This left Greensill in a bit of a sticky situation and ended up being the first in a series of events that has led to it filing for insolvency in the UK today.

Any more commentary about everything that’s happened would be doing a disservice to Rob Smith and his team, who have done a first-class job of shedding light on this entire affair so far, so click here and to see the ‘FT Collections’ page, which has all of the relevant coverage about this ordeal laid out in front of you.

There will be plenty more news about this by next week, so we’ll update you then. We may even delve into Sanjeev Gupta, the British steel magnate who is far too intertwined with Greensill for everyone’s liking.

Anyway, that’s enough fun for one day… onto the articles:

Please Read This Article:

This is an epic story about a botched CIA operation during the Cold War that tried to plant plutonium-powered spyware on several peaks in the Himalayas, in order to observe China testing its nuclear weapons. The agency hired the best American mountaineers of the times, trained them up, and packed them off to India. The plot-twist is that the nuclear spyware was lost after an avalanche caused the mission to go sideways. The device hasn’t been recovered since11. Click here to read the whole piece as it’s a cracker.

Here Are 5 Cool Finance-ey Articles That You’ll Enjoy:

The Hedge Fund That Warned Regulators About Greensill (FT)

Could Inflation Present An Interesting Buying Opportunity (AWOCS)

GE Offloads It’s Aviation Finance Business (Lex)

The Money Made In The ‘Texas Freeze’ (BBG)

Martin Shkreli Is Something Else (Dealbreaker)

Some Other Stuff:

Giving Excel The Love It Deserves (Not Boring)

Barcelona and the Crippling Cost of Success (NYT)

How British American Tobacco’s Cigarettes Are Smuggled Through Mali (OCCRP)

Of Course, Philip Morris Aren’t Missing The Opportunity Either (OCCRP)

Well done for making it through all of that, and, as always, feel free to reach out if you fancy. Also, please feel free to share/forward this email far and wide, as the more the merrier!

On that note, stay safe, stay alert, and see you next week.

AC

For this section, I’ve been inspired by (read: blatantly stolen most of the arguments from) an incredible collaboration between two of my favourite Substack bloggers, Packy McCormick from Not Boring, and Marc Rubinstein from Net Interest. They’ve dug down into the two Silicon Valley goliaths and said some interesting stuff. Check it out here.

Another fun thing about Square is its valuation. Given that the year is 2021 and Square is growing at genuinely impressive rates (140% year-on-year revenue growth in its recent Q3 report) it’s currently got a P/E ratio of ~500 and a market cap of ~$98bn. Nice.

Jack is such a rogue visionary that he regularly has to justify everything that he does, as to the majority of outsiders, everything that he does seems rather weird.

He only eats one meal a day, and he regularly goes on multi-day fasts. He also made waves by announcing his intentions to move to Africa, as well as his decision to spend large periods of time working from a base in French Polynesia. He’s also perfectly happy to call into a senate hearing looking like this:

Jack lives by his own rules and you’ve got to respect it.

Here’s a photo of them on a walk together. Cute.

I know I write about all of this stuff like it’s all fun and games, but it really is sad to see the people who can least afford to lose this kind of money holding the bag at the end of this whole ordeal.

An at-the-money offering is exactly what it sounds like. A company issues more of its shares at the price that it’s currently at. It’s also a dead giveaway that a company thinks its shares are temporarily over-priced.

The SEC shut the offering down quickly, but not quickly enough, as Jefferies had already managed to push $29m of worthless Hertz stock onto some of their clients.

In all honesty, I find this kind of chaos so exciting to spectate, as the stakes are so large, involve so many interesting and important people and the fallout is colossal. What’s not to love.

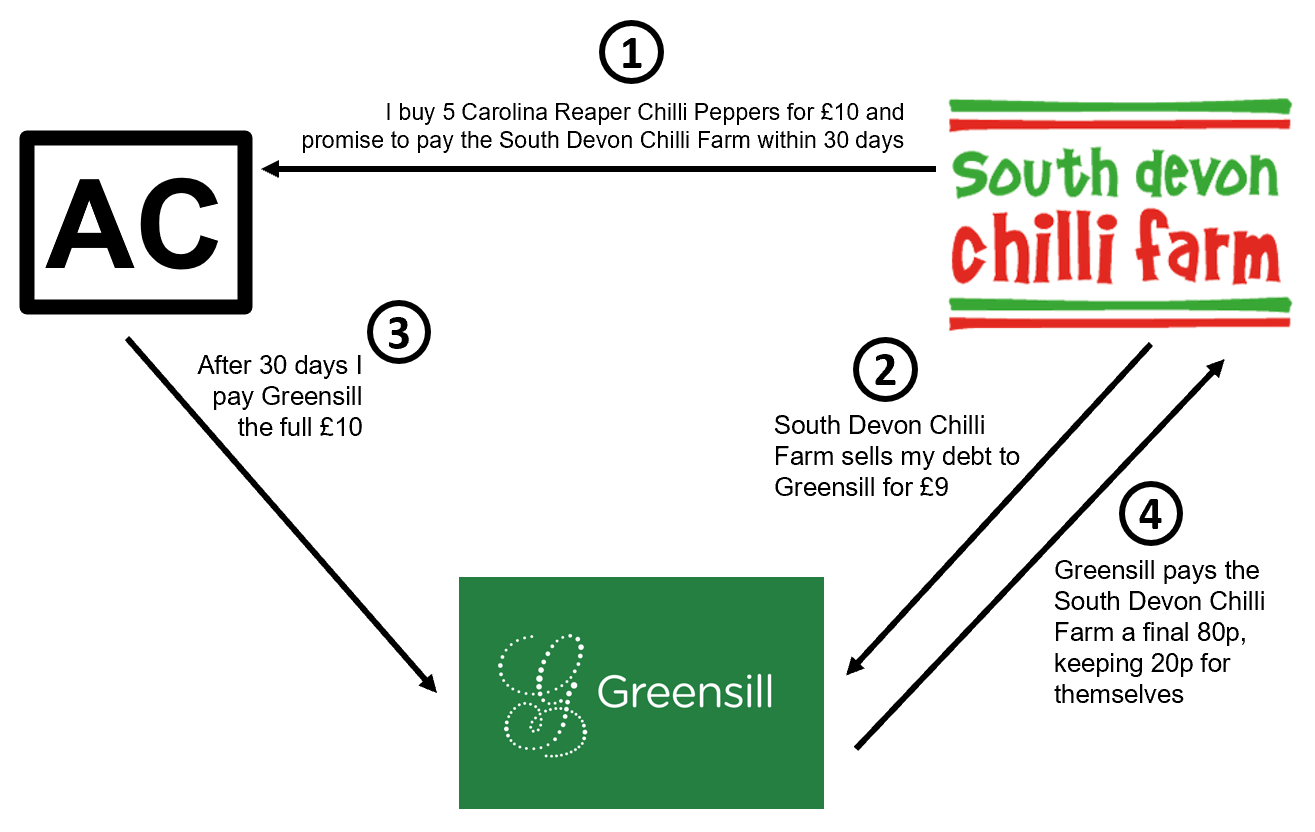

So, let me try and explain what debt factoring is in this overly simplified scenario:

You’re a business that sells… well… literally anything. When you sell something to someone, you will give them an invoice, usually with a contract that says ‘you will pay me the amount owed within 30 days’. Your CFO (chief financial officer) will go ‘okey dokey', let’s add that to the list of people who owe us money within the next year’ (these short-term debts owed to you are called ‘accounts receivables’. This is important to understand).

A week later, your CFO will be checking the numbers, as CFO’s usually do, and they realise that they don’t have enough cash for the upcoming days/weeks/months. They will naturally be quite worried and start considering various options to raise immediate liquidity.

One option that they can consider is to engage in ‘factoring’, which is the act of selling some of those ‘accounts receivables’ to someone else, at a discount. In this scenario, the CFO will choose to receive 90% of the receivable right now from the factoring company and agree that the receivable then be sent to said factoring company. When the invoice finally arrives within those 30 days, the factoring company will then send over ~8% of the total amount back to the CFO and keep 2% for themselves. It’s a great business model, so long as no one goes bankrupt along the way. This risk is called counterparty risk.

If you learn best through visual means, here’s a graph that says exactly this:

Insurers in this scenario protect Greensill from the kind of counterparty risk mentioned above. If they’re in the unfortunate position of one of their counterparties going bang, they need to be paid out in full. This is as much a way to protect investors as it is a way to keep the wheels turning for Greensill.

Sounds like an episode from Archer, doesn’t it! If you haven’t watched Archer, do.